Credit Score: A Key to Financial Empowerment

The dynamic landscape of today’s financial world clearly highlights the importance of credit score for achieving financial empowerment. Grasping the knowledge of credit scores can make a significant difference in managing personal finances and securing a brighter future.

In this blog, the importance of credit score will be discussed, along with its functioning, and ways to improve credit scores. You will also learn about the factors that affect your credit score, helping you take proactive measures to improve it.

What is a Credit Score?

A credit score is a numerical expression of an individual’s creditworthiness. Credit bureaus calculate your score by analyzing your credit history, including the length of your credit history, payment history, total debts, and recent credit inquiries.

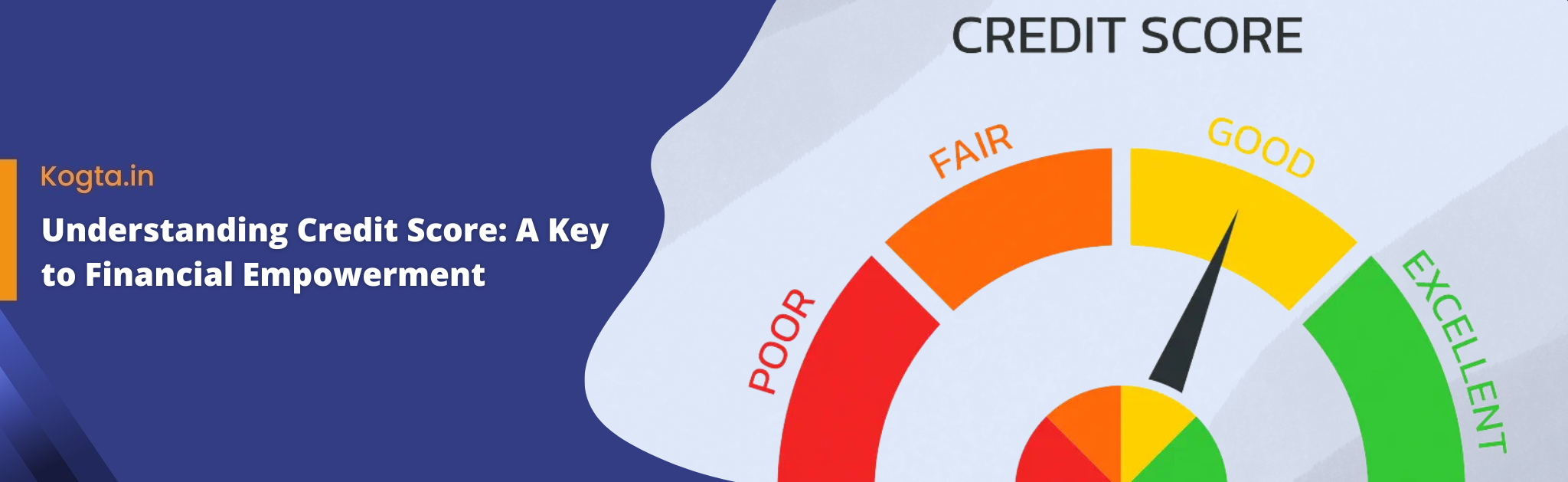

Credit Score Range

A credit score ranges from 300 to 900, with lower scores indicating increased default risk. On the other hand, a higher score indicates a lower risk to lenders, making it easier to obtain credit with favorable terms.

Check the following table to learn more about credit scores ranges:

|

CIBIL Score Range |

Rating |

|

300-499 |

Poor |

|

500-649 |

Average |

|

650-749 |

Good |

|

750-900 |

Excellent |

What is a Good Credit Score?

A good or satisfactory credit scores falls between 650 and 749, while a score of 750 and above is considered excellent. In India, a score above 750 is generally seen as favorable by lenders.

How is Credit Score Calculated?

Credit scores are calculated based on various factors, each contributing differently to the overall score. Check the following breakdown of these factors to know how they impact credit scores:

● Payment History (35%)

Your payment history directly reflects your capability to make repayments on time. When applying for a loan, the lender assesses your repayment history to evaluate the risk of extending credit to you. Hence, make sure to pay your EMIs on time to avoid late payment charges.

● Amount Owed (30%)

This section of credit scores demonstrates the total credit available and used. The credit utilization ratio is a significant factor that determines your creditworthiness. You must ensure to use 30% or below of the credit limit sanctioned.

●Credit History Length (15%)

A longer credit history reflects your ability to responsibly manage credit over time while making timely payments. Hence, maintaining a longer history of credit positively impacts your credit scores and makes you eligible for attractive loan offers.

●Credit Mix (10%)

A diverse credit mix, such as instalment loans, credit cards and unsecured loans, is important for maintaining a higher credit scores. This highlights your strong debt management abilities, increasing your chances of getting approved for a loan.

●Recent Credit Inquiries (10%)

Your credit score is negatively impacted every time you inquire about credit. Multiple credit application in a short period indicates a higher risk to lenders, decreasing your credit score.

Benefits of a Good Credit Score

A satisfactory credit score of 750 and above offers various financial opportunities.

- Lower Interest Rates: A good creditworthiness score makes you eligible for lower interest This saves you money on loans and credit card debt.

- Higher Loan Approval Chances: Maintain a good CIBIL score to help you get approved for loans and credit cards. That is because financial institutions see you as a lower-risk

- Better Credit Card Offers: With a good score, you may qualify for credit cards with higher limits, better rewards, and additional

- Improved Rent Approval: Landlords often check your creditworthiness as part of the rental application A good score can make it easier to secure a rental property.

4 Factors That May Affect Your Credit Scores

- Late or Missed Payments: Payment history covers 35% of your creditworthiness, making it the most significant factor affecting your score. Hence, missing out or delaying EMI payments can significantly lower your score.

- High Credit Utilisation: Spending more than the available credit can lower your score. So, aim to maintain your credit utilisation ratio below 30%.

- Multiple Credit Inquiries: Applying for new credit triggers a hard inquiry on your credit report. As a result, multiple hard inquiries within a short period negatively impact your credit score.

- Errors on Credit Report: Inaccurate information on your credit report, such as incorrect account details or fraudulent activity, can negatively affect your score.

5 Proven Ways to Improve Your Credit Score

Here are some strategies that help to boost your score with consistent effort:

- Pay Your Bills on Time: Ensure that you make all your payments on or before the due Setting up automatic payments or reminders can help avoid late payments.

- Manage Your Debt Obligations: Focus on settling your existing Also, to lower your credit utilization ratio, you must reduce your credit card balances.

- Keep Old Accounts Open: Since the length of your credit history impacts your credit score, avoid closing old credit accounts, even if you don’t use them

- Limit New Credit Applications: Avoid applying for multiple new credit accounts in a short period. Each application generates a hard inquiry, which lowers your credit score.

- Monitor Your Credit Report: 92% of the surveyed Indians emphasise checking credit reports for errors or discrepancies.

Final Word About Credit Scores

An in-depth understanding of credit scores is the key to financial empowerment. A good credit scores makes you eligible for lower interest rates on financial products. Additionally, by checking your credit score, managing your debts responsibly, and staying informed about factors that impact your score, you can take control of your financial future.

Start your journey to financial empowerment by exploring loan options with Kogta Financial. Apply now and take the first step towards a brighter financial future!