Prepayment vs Foreclosure: What’s the Smarter Way to Close a Loan Early?

Confused between loan prepayment and foreclosure? Discover the key differences, tax

implications, and when to use each strategy to save money and close your loan early.

Understanding Early Loan Closure: Why It Matters Now More Than Ever

Loan EMIs are a long-term commitment, often stretching over 15 to 20 years. In this time,

you could pay almost double the principal amount just in interest.

Let’s say you borrow ₹30 lakh at an interest rate of 10.5% for 20 years. Your total repayment

would cross ₹70 lakh, based on standard EMI calculations.

So, it makes sense that many borrowers explore ways to close their loans early—either

through prepayment or foreclosure. But what’s the difference? And which one actually

benefits you more?

This guide breaks it all down—simply and practically.

What Is Loan Prepayment?

Loan prepayment means repaying part or all of your outstanding loan before the scheduled

due date. It’s typically done in small lump sums and doesn’t close the loan completely.

There are two types of prepayment:

- Partial Prepayment: You pay an extra amount (above your EMI) to reduce the

outstanding principal. - Full Prepayment: You repay the entire remaining amount in one go before the end of

the loan term—but without the formalities of a foreclosure process.

Why it matters: In the initial years of your loan, EMIs are interest-heavy. Prepaying during

this phase helps reduce the total interest outflow significantly.

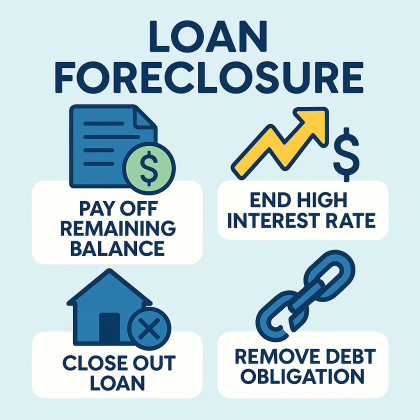

What Is Loan Foreclosure?

Foreclosure, also known as pre-closure, is when you repay the full remaining principal

before the loan tenure ends—and formally close the loan with your lender.

Once foreclosed, the loan is marked “Closed” in your credit report (CIBIL, CRIF), and you’re

no longer under any repayment obligation.

Pro Tip: If you’ve built a good track record of regular EMIs (12–18 months), timely

foreclosure can positively impact your credit score.

Prepayment vs Foreclosure: A Quick Comparison

| Factor | Prepayment | Foreclosure |

| Definition | Partial/full payment before due date | Complete loan repayment before original term |

| Impact on EMI | Reduces EMI or loan tenure | EMI stops completely |

| Paperwork | Minimal | Requires formal closure, NOC, lien removal |

| Frequency | Can be done multiple times | One-time full closure |

| Also Called | Part-payment | Pre-closure or full prepayment |

What About Tax Benefits?

Especially for home loans, early repayments affect your tax deductions under Sections 80C

and 24(b) of the Income Tax Act:

● Principal (Section 80C): Up to ₹1.5 lakh/year

● Interest (Section 24b): Up to ₹2 lakh/year

If you foreclose your loan early, you stop earning these deductions. So, time your foreclosure

wisely—preferably after claiming maximum deductions in the early years.

[Reference: Income Tax Dept. Portal – Section 80C]

Case Study: Rohan’s Decision to Prepay

Rohan, a software engineer in Bengaluru, had a ₹25 lakh home loan at 9.2% interest. In

year 3, he received a ₹2 lakh bonus. Unsure whether to invest or prepay, he consulted his

friend Shruti, a Chartered Accountant.

Shruti explained that since Rohan was still in the interest-heavy phase of his loan, a ₹2 lakh

prepayment could cut down nearly ₹3.2 lakh in future interest and reduce his loan tenure by

1.5 years.

He chose to prepay—and used the tax deductions under Section 24(b) for the remaining

interest.

Read More: What are the Benefits of Paying EMIs on Time?

Are There Any Loan Closure Charges?

Yes, but with clear rules.

As per the RBI’s 2012 directive, banks cannot charge any prepayment or foreclosure penalty

on floating-rate home loans to individuals, provided the loan isn’t for business purposes.

However:

● Fixed-rate loans may still carry a 2–5% penalty

● Business loans or loans to firms can have charges

● NBFCs and private banks may have their own terms

[Read: RBI Notification – Prepayment Charges]

When Should You Prepay vs Foreclose? (Quick Cheat Sheet)

Prepay when:

- You receive periodic bonuses or incentives

- You’re in the early loan phase (first 5–7 years)

- You want to reduce EMI burden or loan tenure

- You plan to claim tax deductions for a few more years

Foreclose when:

- You get a lump sum (property sale, inheritance, FD maturity)

- You’re close to the end of the loan

- You want to sell the property and need clear documentation

- You want peace of mind by being debt-free

Opportunity Cost vs Loan Repayment

It’s tempting to clear debt early—but don’t forget to compare your loan’s interest rate to the

expected returns from investments.

For example:

● If your loan costs 8.5% interest

● And your investments (e.g., mutual funds or ELSS) are returning 12–14%.

You may be better off investing and keeping the loan running—especially if you’re claiming

tax deductions.

Post-Foreclosure Checklist

Once your loan is closed, don’t stop there. Here are your must-dos:

- Collect your No Objection Certificate (NOC) from the lender

- Retrieve original property documents (or loan agreement, if vehicle loan)

- Get an Encumbrance Certificate for property loans

- Check your credit report (CIBIL or CRIF) to ensure loan is marked “Closed”

- Remove lien from the property or vehicle RC

[Check Your Score: CIBIL Free Score Portal]

Final Words About Prepayment Vs Foreclosure

Choosing between prepayment and foreclosure depends on your financial goals, current

cash flow, and loan type. There’s no one-size-fits-all answer—but there’s always a smarter

way.

Take time to understand your interest outflow, check your investment returns, and plan your

repayment journey accordingly. Lenders like Kogta Financial and others offer flexible

terms—but how you manage the loan can make or break your savings.

If used wisely, both prepayment and foreclosure can become powerful tools in your personal

finance playbook.